The GCC’s mobile connected devices market expanded 16.7% year on year in Q1 2015 to record shipments of over 8.7 million units, according to the latest insights announced today by global consulting services firm International Data Corporation (IDC). Comprising shipments of smartphones, tablets, and portable PCs to Saudi Arabia, the UAE, Bahrain, Oman, Qatar, and Kuwait, the market’s growth was spurred by lower average selling prices (ASPs), increasing penetration levels, and the continued efforts of new vendors to make their way into the region’s markets and claim a piece of the pie.

The GCC’s mobile connected devices market expanded 16.7% year on year in Q1 2015 to record shipments of over 8.7 million units, according to the latest insights announced today by global consulting services firm International Data Corporation (IDC). Comprising shipments of smartphones, tablets, and portable PCs to Saudi Arabia, the UAE, Bahrain, Oman, Qatar, and Kuwait, the market’s growth was spurred by lower average selling prices (ASPs), increasing penetration levels, and the continued efforts of new vendors to make their way into the region’s markets and claim a piece of the pie.

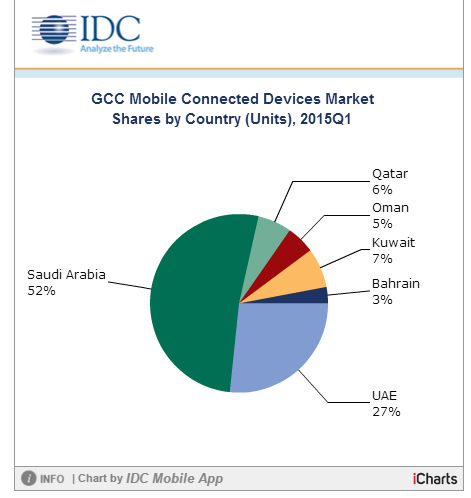

The Saudi market accounted for over 50% of the mobile connected devices shipped across the GCC in Q1 2015, with the UAE ranking second with approximately 26% share of the market’s volume. Saudi Arabia’s dominance can be attributed to its sheer size and the rapid rate at which IT adoption is occurring across the kingdom.

Greater growth in the GCC was hindered by the negative impact of political and economic events in Kuwait, which recorded the only negative performance in the region’s mobile connected devices, with shipments falling 10% year on year. The factors that contributed to the Kuwaiti market’s decline included internal government issues that resulted in the delay of various infrastructure projects (including IT), as well as market saturation in the smartphone, tablet, and portable PCs categories.

Qatar recorded the region’s highest year-on-year growth in Q1 2015, with shipments up by more than 45%, driven by ongoing projects and initiatives associated with enhancing the country’s infrastructure and its continuing preparations for the FIFA World Cup in 2022. IDC expects the GCC’s mobile connected devices market to continue growing over the coming years, with shipments forecast to increase from a total of 35 million units in 2015 to 45 million in 2019, representing a compound annual growth rate (CAGR) of 7.6%.

The GCC smartphone market grew 21% year on year in volume terms during Q1 2015, taking share away from the feature phone category, which declined 14% over the same period. This growth now brings the smartphone market’s share in the region to just under 77%. Qatar and the UAE recorded the highest growth rates in the region. “The sheer magnitude of declining ASPs is a major factor that continues to drive the adoption of smartphones, with 500% growth seen in shipments of smartphones priced below $150,” says Saad Elkhadem, a research analyst at IDC Middle East, Africa, and Turkey. “This is a trend is being driven by vendors like Samsung, Lenovo, and Huawei, and is set to continue over the coming quarters.”

The region’s tablet market recorded a year-on year growth of 9.9% in Q1 2015. This is in stark contrast to the performance of the overall Middle East and Africa market, which suffered its first ever decline over the same period. “The growth experienced in the GCC market was mainly due to a strong push from up-and-coming vendors such as Lenovo, Huawei, and Xtouch, providing an arena for lower ASP’s to flourish,” says Feras Ibrahim, a research analyst at IDC Middle East, Africa, and Turkey Additionally. “In country terms, the principal driver of this growth was the notable performance of the Saudi market, where the consumer segment grew rapidly.”

In contrast, the GCC’s portable PC market experienced a year-on-year decline of 6.4% in Q1 2015. The major market inhibitor was the continuing shift towards tablets and smartphones, with this trend being felt more strongly in the consumer segment than in the commercial space. The UAE suffered the biggest decline in the region, mainly due to the aforementioned cannibalization of the market by tablets and smartphones and the slowdown in tourism that the country saw in comparison to the same quarter of 2014.

Source:IDC