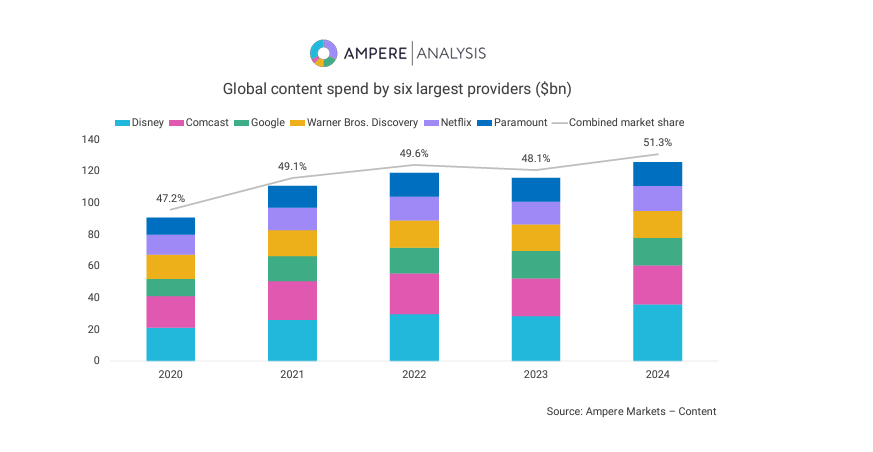

Disney, Comcast, Google, Warner Bros. Discovery, Netflix, and Paramount combined will invest $126bn in content this year

While recent market challenges have impacted the TV and Film production landscape, spending across the top six global content providers has grown since the pandemic. Ampere’s latest intelligence shows that spending across these groups will reach a new high in 2024 and account for 51% of the total content spend landscape, up from 47% in 2020.

Key findings

• Despite announced cutbacks amongst its linear and theatrical brands, Disney remains the largest contributor to the media landscape at 14% of global investment in TV and film content in 2024. This has been supported by the full acquisition of Hulu at the beginning of 2024, adding an additional $9bn in to Disney’s spend total.

• Original content spend remains the leading spend type across these providers, accounting for over $56bn in investment and 45% of their total spending since 2022.

• Google’s contribution to the content market comes via YouTube, and investment in programming through its revenue-sharing arrangements with content creators. While a different entity to other TV and Film groups, YouTube continues to build its global presence through partnership deals with major content owners, making it the third largest contributor to the content landscape.

• Besides YouTube’s more unique proposition, Netflix is the top investor in global streaming content. It has averaged a total of $14.5bn in annual investment in original and acquired programmes since the pandemic. Further growth is expected in 2025 through the acquisition of Sports Rights for NFL matches and WWE entertainment

• In total, $40bn of the $126bn is currently spent on these six operators’ subscription streaming services (including Disney+, Peacock, and Paramount+). This highlights the growing importance of these platforms as audiences move away from linear television in favour of the convenience and expansive catalogues available via streaming.

• Despite production shutdowns caused by the US writers’ and actors’ strikes, streamers have continued to support the production landscape by pivoting towards more global strategies. International (non-US originating) programming accounts for 40% of Paramount+’s and 52% of Netflix’s spend in 2024. Such content is typically cheaper to produce, and effective in motivating new and niche audiences to subscribe to a platform, supporting revenues.

Peter Ingram, Research Manager at Ampere Analysis says: “Ongoing investment by major studios and streaming platforms into new programming will continue be key to keeping audiences engaged and entertained. We can expect that the content landscape will see low level growth in 2024 as production schedules recover from disruptions caused by the pandemic and the writers’ and actors’ union strikes. Looking forward however, while these top six providers will continue to account for the majority of spend, overall growth will plateau as companies look to refocus their output. This will include limiting commissioning volumes and prioritising strategic investments and profitability to counter the current challenges of the media market.”