While technology is eliminating jobs, it is also creating them. But filling these new roles is the next talent challenge.

While technology is eliminating jobs, it is also creating them. But filling these new roles is the next talent challenge.

Much has been made of the potential of recent leaps in technology to automate many jobs out of existence. From taxi drivers to accountants, some studies suggest that as many as half of existing jobs could be automated. Routine work is clearly disappearing, but the fears of mass unemployment at the hands of machines could be overblown. For example, research by the McKinsey Global Institute suggests that around 20 percent of occupations could see around 70 percent of their activities automated, meaning a slightly less worrying future, where automation is more likely to take the form of augmentation.

But this doesn’t mean technology and talent development should be approached with any less urgency. While technology is creating jobs as well as destroying them, there is often a disconnect between the skills needed and the skills that employees and graduates currently have. It’s a massive challenge for our educational systems currently based on the factory model, turning out young adults who are equipped for routine jobs that are fast disappearing. And the workplace is taking on different forms, evidenced in new models of employment, such as contingent and project-based work. In Europe and the United States, as much as 30 percent of the population earns all or part of their income as free agents in the gig economy, offering their skills to multiple employers through collaborative computer-based platforms.

As we observe in this year’s Global Talent Competitiveness Index report, countries that lead the way in talent competitiveness have taken a multipronged approach to dealing with recent advances in technology and fostering the talent necessary to leverage it.

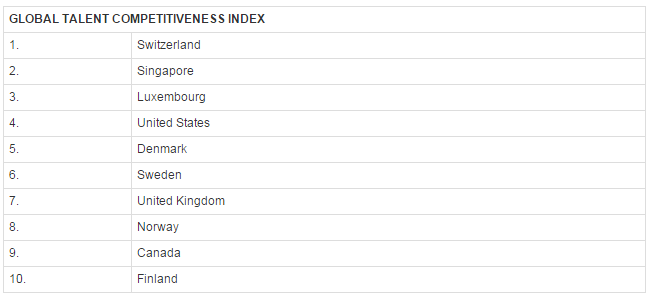

The winners

The index, which measures the extent to which countries attract, grow and retain talent and how they translate their efforts into output, puts Switzerland on top, followed by Singapore and the United Kingdom. While Switzerland excels at offering an ideal economic environment and retaining domestically-developed talent, Singapore leads the way in attracting and enabling its global talent pool.

Singapore is a particularly relevant case study in this year’s report because it takes an ecosystem approach to talent development in the face of technological change. Its regular “learning journeys”, organised by the Ministry of Manpower, along with relevant agencies such as the Workforce Development Agency and the Infocomm Development Agency, aim to enlighten small businesses to new possibilities in automation to enhance productivity and reduce dependence on foreign labour. One of its most recent journeys introduced smart technologies in the cleaning and services sector such as robotic floor cleaners and droids that can fold napkins to speed up the work of hotel staff. The learning journeys are only the beginning. They are accompanied by various government grants and incentive schemes, such as the Lean Enterprise Development Scheme, a cross-agency taskforce that makes resources and funding available to local small companies looking to augment their workers with technology.

Singapore is a particularly relevant case study in this year’s report because it takes an ecosystem approach to talent development in the face of technological change. Its regular “learning journeys”, organised by the Ministry of Manpower, along with relevant agencies such as the Workforce Development Agency and the Infocomm Development Agency, aim to enlighten small businesses to new possibilities in automation to enhance productivity and reduce dependence on foreign labour. One of its most recent journeys introduced smart technologies in the cleaning and services sector such as robotic floor cleaners and droids that can fold napkins to speed up the work of hotel staff. The learning journeys are only the beginning. They are accompanied by various government grants and incentive schemes, such as the Lean Enterprise Development Scheme, a cross-agency taskforce that makes resources and funding available to local small companies looking to augment their workers with technology.

Another box Singapore ticks in the GTCI is in education. Its recent PISA scores – which put Singaporean children three years ahead of their American peers in mathematics – reflect Singapore’s forward-looking education system. Singaporean children don’t start primary school until age 6, spending their early years in play-based kindergartens. At school, the curriculum encourages students to ask questions about things they see around them and to maintain that curiosity, which aids lifelong learning. The school system also offers coding classes at a very early age, adopts many digital delivery channels and gives teachers 100 hours a year for training.

The importance of ecosystems, which runs consistently throughout our report, cannot be underestimated. The standouts of the GTCI use public-private partnerships to surmount and exploit the challenges of building the new economy.

Urban advantage

For the first time, this year’s report also includes an index on cities (Global City Talent Competitiveness Index), because talented individuals tend to focus less on which country to go to and more on which city to live in. Cities are therefore, increasingly engaging in their own means to attract, retain and develop talent, making them a crucial part of talent competitiveness. Following a similar methodology to the GTCI ranking, the GCTCI ranking tells us that the leaders, Copenhagen, Zurich and Helsinki, in addition to being consistently high performers in quality-of-life indicators, have strong physical and information infrastructure and strong international links.

Another interesting finding is that despite the presence of the big metropolises, such as Paris and Los Angeles in the leading group, the average population of the top 10 cities is around 400,000, demonstrating that the trend of highly educated individuals gravitating to large cities is changing.

As talented individuals can increasingly operate from anywhere, physical and technical connectivity and quality of life are competitive advantages for smaller cities. The importance of clusters cannot be underestimated. Ireland’s ICT clusters are a distinct advantage; so is Eindhoven, which is home to Philips.

Moving up the value curve

One consistent finding we see across every annual edition of the report is that the top positions of the GTCI continue to be filled by high-income countries. Those able to deploy capital in innovation, entrepreneurship and collaboration lead the index. Countries that continue to rely on labour-intensive industries at the expense of high-value industries and talent will struggle to move up the index. The BRICS countries are not getting stronger with scores declining all round this year, shown first in Brazil (81st). China (54th) puts in a good showing in formal education, but lets itself down in attraction. India (92nd out of 118) too is not able to retain, let alone attract, talent.

The rise of technology brings new challenges to emerging markets as rich countries become more self-sufficient with robots and automation. Adidas is about to do something unheard of in the clothing and shoes business for some time: bring shoe production back to Germany. With advances in robotics, it can make a pair of trainers in five hours, much less than the seven weeks it currently takes in its Asian supply chain.

As advanced economies struggle to cope with immigration, the ability to “reshore” jobs is a blessing for policymakers, as shown by some announcements made by President-Elect Donald Trump in the U.S. With resources and financing channelled to innovation in developed economies, emerging countries may lose their main source of competitive advantage, namely cheap labour for outsourcing. Even China is waking up to robotics and is set to lose more jobs to automation than to competition from cheaper countries. But not all manufacturing jobs will head back home to developed economies. Policymakers here, as in the developed world, also need to think beyond automation as labour advantage gives way to digital advantage. Digital tools enable people anywhere to participate in global trade, which is carried less by ship and more by the internet. Both for cities and nations, connectivity will be crucial, along with a workforce educated to suit the new economy, facilitated by government, business and educational institutions.

Written by Paul Evans, Academic Director of the INSEAD Global Talent Competitiveness Index, Emeritus Professor of Organisational Behaviour and the Shell Chair of Human Resources and Organisational Development Emeritus at INSEAD.